This article was paid for by a contributing third party.More Information.

IFRS 9 versus IAS 39: Opportunities in changes to hedge accounting

With financial reporting in a state of flux amid the introduction of several new accounting standards, many corporates may feel overburdened by the need to ensure accounting compliance to take full advantage of IFRS 9 from the point of adoption. Robert van Wijk from the market risk advisory group at Societe Generale, explains the opportunities presented by changes to hedge accounting under the new standards

At a time when financial reporting is undergoing significant transformation, with International Financial Reporting Standard (IFRS) 9, IFRS 15 and IFRS 16 coming into effect concurrently, corporate treasurers could be forgiven for postponing sweeping reviews of their risk management policies. However, changes to hedge accounting under IFRS 9 represent an unprecedented opportunity to review and amend existing hedges, and rethink how risks across asset classes should be managed.

While not everyone will welcome the additional reporting obligations the new standard brings – particularly corporates with few and simple hedges that will nevertheless be required to update their hedge accounting disclosures to be IFRS 9-compliant (regardless of whether they adopt IFRS 9’s hedge accounting requirements from the outset) – by and large, IFRS 9 looks set to change the landscape of corporate risk management for the better.

Transition to hedge accounting

The three tenets driving this transformation to hedge accounting under IFRS 9 are the removal of burdensome quantitative assessments such as the so-called ‘80–125% effectiveness test’, derivatives qualifying as hedged items under the principle of aggregated exposures, and certain sources of ineffectiveness now being treated as a cost of hedging that can be deferred in equity before being recycled through the profit and loss (P&L) account in line with the underlying hedged item – such as time value of options, swap points and cross-currency basis spreads.

By moving only to a prospective test to determine the economic relationship between the hedged item and the hedging instrument, IFRS 9 enhances corporate treasurers’ toolboxes of derivatives eligible for hedge accounting. For example, options with knock‑in or knock‑out features will display ineffectiveness as these features are not replicated in the hedged item, but hedge accounting may still be applied since the features do not challenge the economic relationship.

The range of situations in which hedge accounting may be applied is also improved, with hedge accounting extended to proxy hedging. Under International Accounting Standard (IAS) 39, hedging an exposure via a proxy carried significant accounting risk if the proxy relationship changed. For example, hedging the largest component of an emerging market currency pegged to a basket was possible if that component fulfilled the effectiveness requirement – the 80–125% test. However, if that country’s central bank changed the weight of the key component, with the consequence of being out of the 80–125% test, the hedge relationship would be de-designated with 100% of the hedge mark-to-market (MtM) going through P&L. Under IFRS 9, the hedge ratio can be adjusted to reflect the new economic relationship, with only the ineffective part rebalanced through P&L.

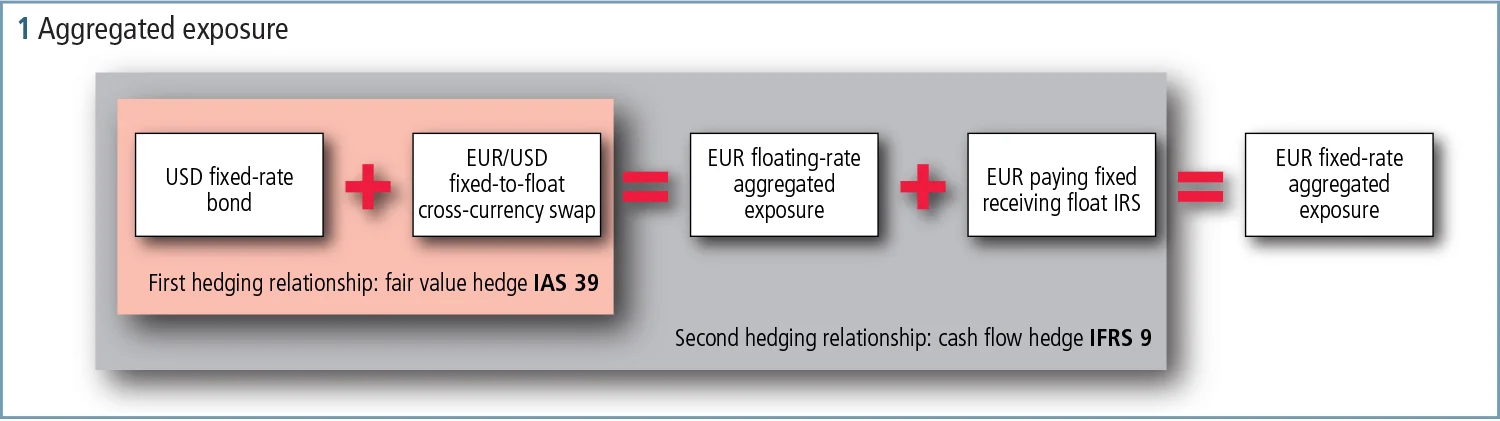

Flexibility will be much improved under IFRS 9 thanks to the ability to hedge aggregated exposures. One likely scenario where this provides a clear improvement over IAS 39 is in the hedging of fixed-rate foreign currency debt hedged back to a corporate’s functional currency using a cross-currency interest rate swap. Under IAS 39, a fixed-to-floating cross-currency swap was hedge-accountable as a fair value hedge, but subsequently entering into an additional interest rate swap to switch from a euro floating-rate aggregated exposure into a euro fixed rate was not eligible for hedge accounting. Under IFRS 9, this hedge can be classified as a cash flow hedge of the first aggregated exposure.

Were the corporate to modify its interest rate exposure again at a later date, a subsequent derivative could be classified as the hedging instrument for the second aggregated exposure, and so on (see figure 1). Conceptually, this paves the way for much more dynamic management of interest rate risk than has historically been witnessed.

Restructuring hedges

Restructuring firm hedges with large MtM will also be easier to account for under IFRS 9. Many European industrials with multibillion US dollar-denominated capital expenditures that put in place long-dated hedging with foreign exchange forwards before mid-2014 would have sat on significantly positive MtM after the strong appreciation of the US dollar in the second half of 2014. Unfortunately, it was difficult for them to capitalise on the market opportunity to restructure hedges since crystallised gains would have hit P&L – policy often dictates this is unacceptable. Under IFRS 9, the hedging relationship would be maintained with gains kept in other comprehensive income (OCI). However, the cash proceeds on restructuring could temporarily boost liquidity until capital expenditure payment dates, or could be reinvested in higher-yielding assets.

Fast-forward to today, and the reverse scenario is gaining increasing interest. With negative euro deposit rates proving a big challenge for corporates awash with cash, the allure of restructuring deeply negative MtM hedges to par in a hedge accounting-friendly way under IFRS 9 is growing. For example, excess cash flows can be used to restrike euro-receiver cross-currency swaps, with coupons paid as normal but on the new notional, which would be lower in US dollar terms, and the upfront payment amortised in OCI as a cost of hedging. Furthermore, the corporate may be able to benefit from some capital release on the trade, as well as freeing up its credit lines with banks for new hedges.

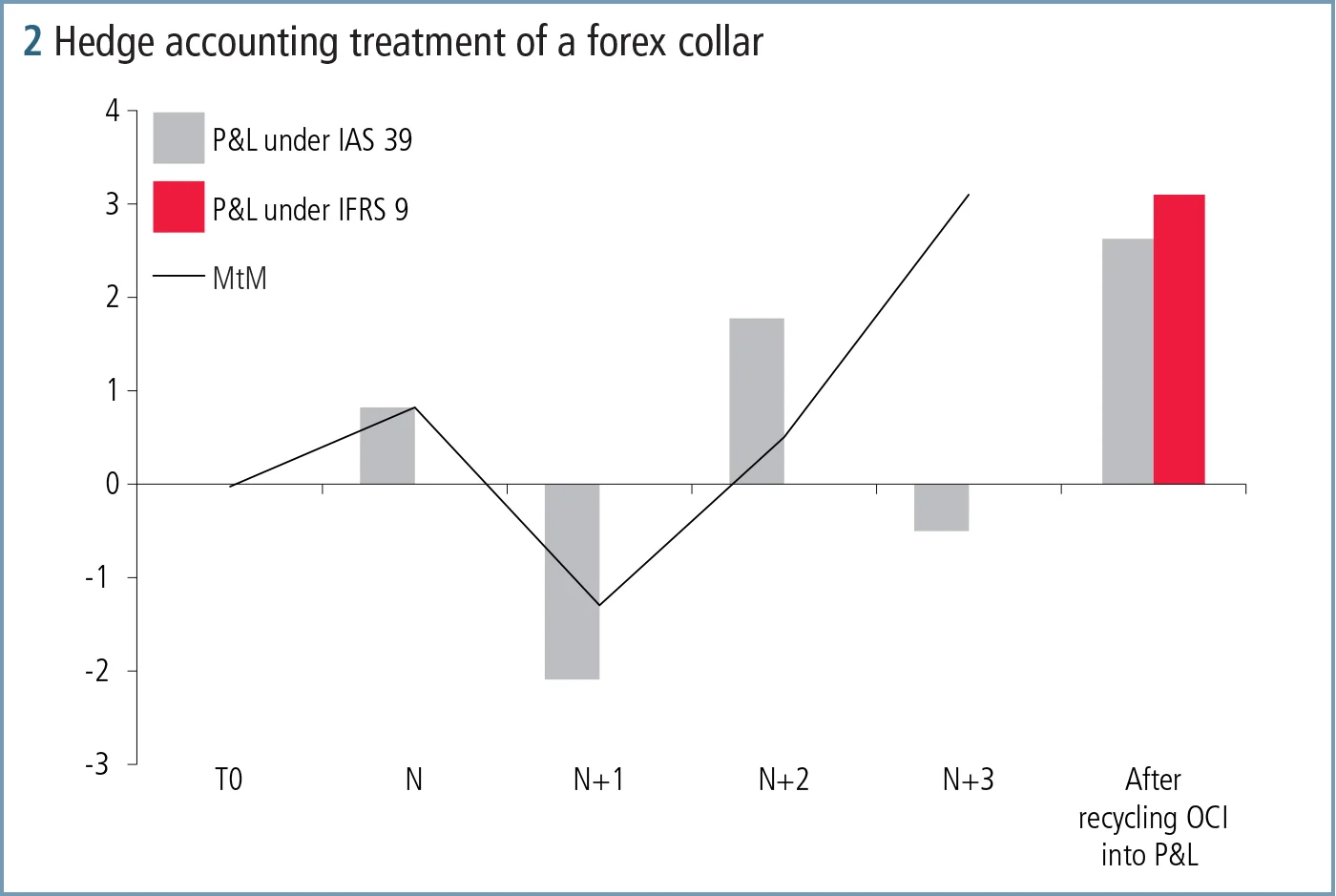

The ability to account for option time value as a cost of hedging opens the door to a multitude of amendments to forex hedging strategies. While many corporates will still not hedge transactional currency risks with vanilla forex options in the absence of a budget for option premium, one of the key barriers to hedging with zero premium risk reversals has been removed. Instead of recording changes in time value as ineffectiveness and recycling this through P&L at each reporting date, time value fluctuations can be recorded in OCI if hedge accounting is applied. In the case of the zero-premium structure, the only P&L impact will be the intrinsic value of the derivative at maturity.

“We have been very busy this year engaging with clients reviewing their forex hedging policies,” notes Antoine Jacquemin, global head of the market risk advisory group at Societe Generale in London. “As a consequence of time value fluctuations going through in P&L under IAS 39, many corporates were unable to get internal approvals to trade simple optional structures, despite the economic benefits. Thanks to improved hedge accounting compliance under IFRS 9, we see a lot of our clients rewriting their hedging policies with risk management truly at the core.”

Not limiting itself to option time value, IFRS 9 also permits the cross-currency basis to be accounted for as a cost of hedging, excluded from the hedging relationship and amortised over the life of the swap. Fair-value hedges of fixed-rate bonds in foreign currency back into local floating rates should no longer be subject to the same risks of disqualification seen during the global financial and eurozone sovereign debt crises, removing a significant headache for treasury teams and more closely aligning hedge accounting with market structure and risk management practices.

Conclusion

Perhaps the most powerful impacts of IFRS 9 are seen when several of these positive changes are combined into a single hedge. Today, a treasurer has the ability to consider taking advantage of favourable market moves in a multitude of scenarios with a much wider range of instruments than before. One example of this would be with overlay strategies on top of existing exposures, which tend to be more hedge accounting-friendly under IFRS 9. Hedging a component of an aggregated exposure – designated as the hedged item – with, for example, a combination of options, would pose few problems under IFRS 9, while under IAS 39 hedging a derivative with a derivative would not have been permitted. Secondly, the significant time value decay of a potentially long-dated optional structure, which under IAS 39 could have introduced significant P&L volatility, would not impact P&L over the life of the hedging relationship.

Agile hedging strategy re-evaluation looks set to feature more and more as key stakeholders become more comfortable with IFRS 9.

Marc Burdal, cross-asset structurer and IFRS specialist at Societe Generale in Paris, thinks hedge accounting under IFRS 9 is a big improvement: “The new rules put hedge accounting closer to risk management. For many of our listed clients where hedge accounting is a must, IFRS 9’s greater flexibility increases the chance of eligibility as a hedged item, which in turn means more risks will qualify for hedge accounting. Ultimately, this will benefit how our clients manage their exposures not only across the traditionally hedged asset classes such as forex, rates and commodities, but also in new areas such as inflation.”

Contact

Robert van Wijk, Market Risk Advisory, Interest Rate & FX Derivatives

Societe Generale does not provide investment, legal, accounting or regulatory advice in connection herewith and nothing herein should be construed as investment, legal, accounting or regulatory advice. Before making any accounting-related decision, you should discuss such decision with your accounting specialist or auditors. You must determine the accounting and regulatory treatment of any investment you make, Societe Generale provides no advice nor gives any guarantee in this regard.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@risk.net